The battery technology for two-wheel and three-wheel electric vehicles is currently in a critical transition period. The industry is undergoing a systematic transformation driven by policy guidance, the entry of major players, and the upgrading of user demands. Generally speaking, the technological evolution shows a clear gradient: traditional lead-acid batteries are accelerating their exit from the market; lithium batteries represented by lithium iron phosphate (LFP) are entering a stage of large-scale popularization; while sodium-ion batteries and ultra-fast charging technologies and other cutting-edge directions are at the critical point of industrialization, and are expected to support the demands of future diversified application scenarios.

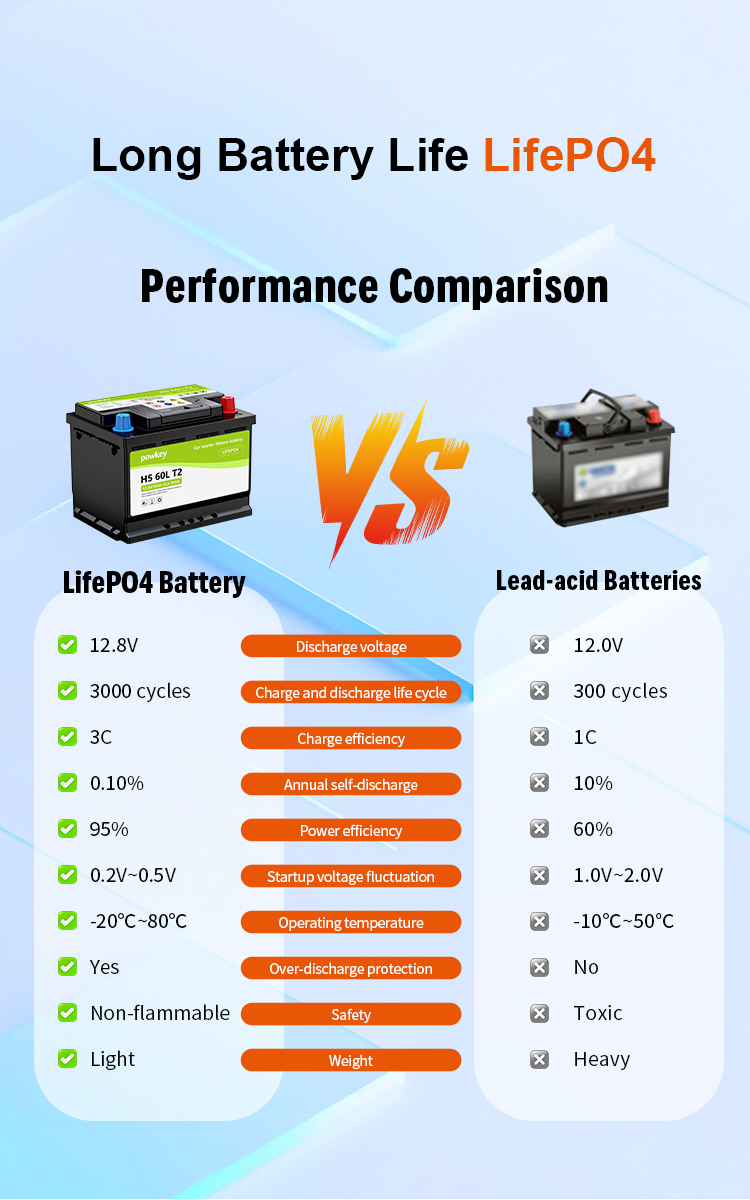

Lead-acid batteries still hold approximately 80% of the market share, maintaining their position with extremely low raw material costs (about 16,800 yuan per ton), mature and stable manufacturing processes, and a relatively high recycling rate. However, their inherent drawbacks are becoming increasingly prominent – low energy density, heavy weight, short cycle life (typically 2-3 years), and poor low-temperature performance (capacity significantly drops below 0°C). Coupled with stricter environmental regulations and strategic pressure from leading enterprises, they are entering an irreversible decline.

Lithium batteries (mainly lithium iron phosphate): have become the most promising mainstream technology route at present. Compared with lead-acid batteries, they weigh about one-third of the latter, have a significantly longer cycle life (generally providing a warranty of five years or more), and can still maintain over 95% of their available capacity at -20°C. Although the current unit cost is still higher than that of lead-acid batteries (about 33,300 yuan per ton), with the strategic investment of leading battery manufacturers such as BYD and CATL, they have entered a period of rapid growth and continuous cost reduction.

Sodium-ion batteries are widely regarded as an ideal candidate technology to replace lead-acid batteries in the medium to long term. Their core advantages lie in low raw material costs, abundant resource reserves, excellent low-temperature performance, and high compatibility with existing lithium battery production lines. Currently, the main bottlenecks are that their energy density is slightly lower than that of mainstream lithium iron phosphate batteries, and the industrial chain is not yet fully mature. With multiple enterprises completing pilot tests and initiating mass production plans, it is expected that a commercial breakthrough will be achieved within the next 2 to 3 years.

Graphene batteries: There is significant conceptual confusion in the current market. The so-called “graphene batteries” are mostly marketing terms. The actual products have not broken through the auxiliary role of graphene as a conductive additive and have not yet achieved an electrochemical system with graphene as the active main body. The industry consensus is that there are no truly mass-produced graphene batteries in the two-wheeler field at this stage. The products sold on the market that are labeled as such are essentially “lead-acid batteries doped with graphene materials”, whose performance improvement is limited and do not have a technological generational advantage.

Three major structural driving forces are reshaping the industrial landscape.

Policy rigid constraints: The “Safety Technical Specification for Electric Bicycles” (GB 17761-2025), which was officially implemented in September 2025, sets mandatory requirements for the upper limit of the whole vehicle mass (≤55 kg) and safety indicators such as battery thermal runaway protection and overcharge protection. This standard has substantially raised the technical entry threshold, compelling the entire vehicle manufacturers to comprehensively shift towards high energy density, lightweight, and high safety lithium battery solutions.

- Strategic Downward Shift of Leading Enterprises: The deep involvement of BYD and CATL, the two global leaders in power batteries, is the core variable in this round of transformation.

- Relying on its automotive-grade Blade Battery technology platform, BYD has implemented a “technology downscaling” strategy, launching a series of LFP batteries specifically designed for two-wheel and three-wheel vehicles. It focuses on long cycle life, intrinsic safety, and wide temperature range adaptability, and explicitly proposes the industrial upgrade proposition of “lead-acid exit, lithium iron phosphate start”.

- CATL, through its holding subsidiary Amperex Technology Limited (ATL), has carried out “scenario-based deep customization”, collaborating with leading brands such as Ninebot and NIU Electric, to strengthen the structure and optimize the BMS algorithm in response to typical operating conditions such as high-frequency vibration, water immersion riding, and frequent start-stop. This has driven the evolution of battery systems from general-purpose components to dedicated ones.

- Terminal user demand iteration: The high-intensity user group represented by food delivery riders (with an average daily travel distance of over 80 km and a charging frequency of 2-3 times per day) is continuously driving the upgrade demands for battery range, cycle durability, fast charging capability, and all-weather reliability. This real-world feedback has become a key input for technology route selection and product definition.

📌 Practical Shopping Tips

- Budget-oriented users (daily commuting ≤ 80 km): Lead-acid batteries still offer significant cost-effectiveness in the short term and can meet basic transportation needs; however, users should be aware of their shorter replacement cycle and reduced range in winter.

- Value-oriented users: It is recommended to choose models equipped with lithium iron phosphate batteries from first-tier manufacturers such as BYD and New Energy. Although the initial purchase cost is slightly higher, the “battery and vehicle same lifespan” design (where battery life matches the vehicle’s life cycle), better low-temperature performance, and lower maintenance costs over the entire life cycle make them more economical in the long run.

- Technologically forward-looking users: They can pay close attention to the mass production progress of sodium-ion batteries and the application pace of new-generation fast-charging technologies (such as Wanxiang 123’s “Flash Charge Ultra” platform, which can charge to 80% SOC in 5 minutes as tested). These technologies are expected to further alleviate charging anxiety and drive down the prices of terminal products within the next 2-3 years.

🔮 Outlook: Moving from Price Competition to Technological Upgrading

With leading enterprises like BYD and CATL, which possess full-stack technological capabilities, deeply involved, the competitive logic of the two-wheeler battery industry is undergoing a fundamental transformation – shifting from the past cost-centered homogeneous price war to a technology-driven competition based on safety, energy density, scene adaptability, and intelligent management capabilities. It can be foreseen that the next generation of two-wheeler electric vehicles will be more lightweight, have more reliable endurance, better adaptability to extreme environments, and possess higher system-level reliability and sustainability.

{kind=link}

{kind=link}

{kind=link}